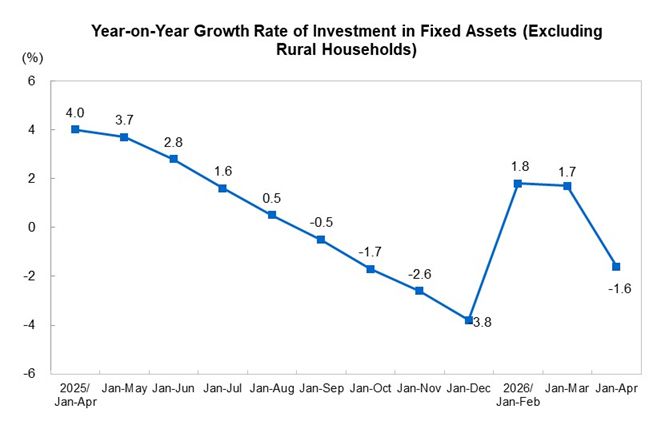

China's fixed-asset investment fell 4.1% year-on-year in the first four months of 2026, the steepest drop since the pandemic, driven by a 16.2% collapse in property investment. The headline number hides a split: while services-sector and property capex craters, spending on rail, ship, and aerospace manufacturing surged over 20%.

Mechanism. The decline traces to a fiscal chain reaction. Local governments rely on land sales for a large share of their budgets; as land revenue collapsed, so did their capacity to fund schools, hospitals, and other public goods. Meanwhile, private developers are structurally trapped: pre-sale cash is escrow-restricted to individual projects, so illiquid developers cannot reallocate capital even from healthier sites, forcing stalled deliveries and forced discounting. On the other side, land-auction data confirms a quiet handover: in 2025, financing-vehicle land purchases fell 15%, while state-owned enterprises raised their share of land spending to half the market, redirecting capital toward central-government strategic-industry priorities.

Investment insight. The real opportunity lies in the widening gap between real estate and localities tied to strategic-industry buildout (rail, shipbuilding, aerospace clusters, which grows 23.6% yoy) versus those tied to ordinary consumer housing demand. This divergence is likely underpriced because most investors access “China property” through blended vehicles (e.g., developer bonds, national indices) that structurally weight toward the shrinking side, while state-linked financing vehicles’ conglomerated, hardly-disclosed structures make it nearly impossible to isolate the winning segment directly.

Risks. The thesis assumes Beijing keeps directing capital toward strategic sectors while starving general local-government spending. If broad fiscal support for localities returns, the divergence narrows rather than widens.

Prediction. Watch the land-acquisition share of top SOEs (currently ~50%, per CRIC data): if it climbs above 60% by Q1 2027, the bifurcation is intensifying.